Linear Regression with Multiple Variables.

1. Multivariate Linear Regression

I would like to give full credits to the respective authors as these are my personal python notebooks taken from deep learning courses from Andrew Ng, Data School and Udemy :) This is a simple python notebook hosted generously through Github Pages that is on my main personal notes repository on https://github.com/ritchieng/ritchieng.github.io. They are meant for my personal review but I have open-source my repository of personal notes as a lot of people found it useful.

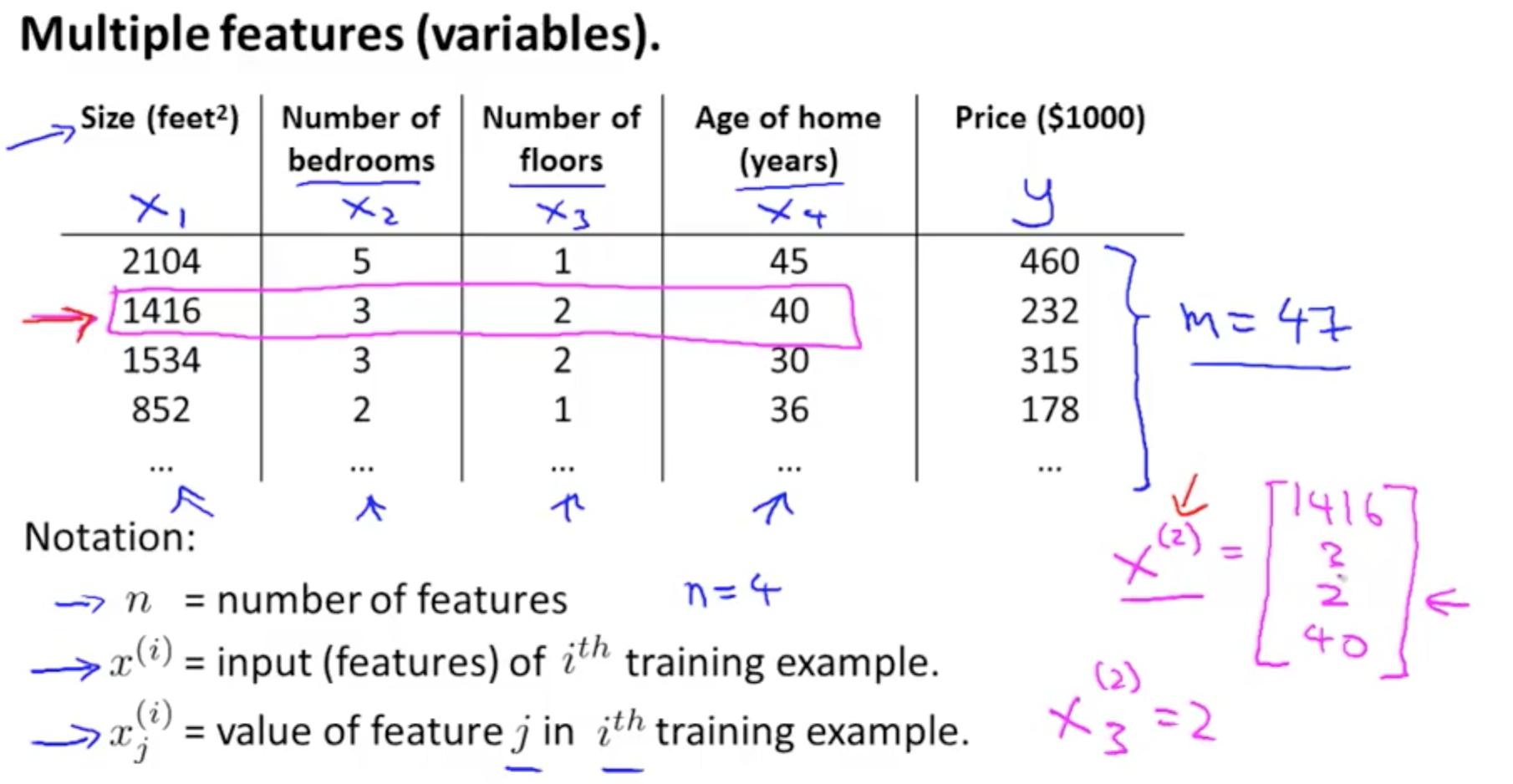

1a. Multiple Features (Variables)

- X1, X2, X3, X4 and more

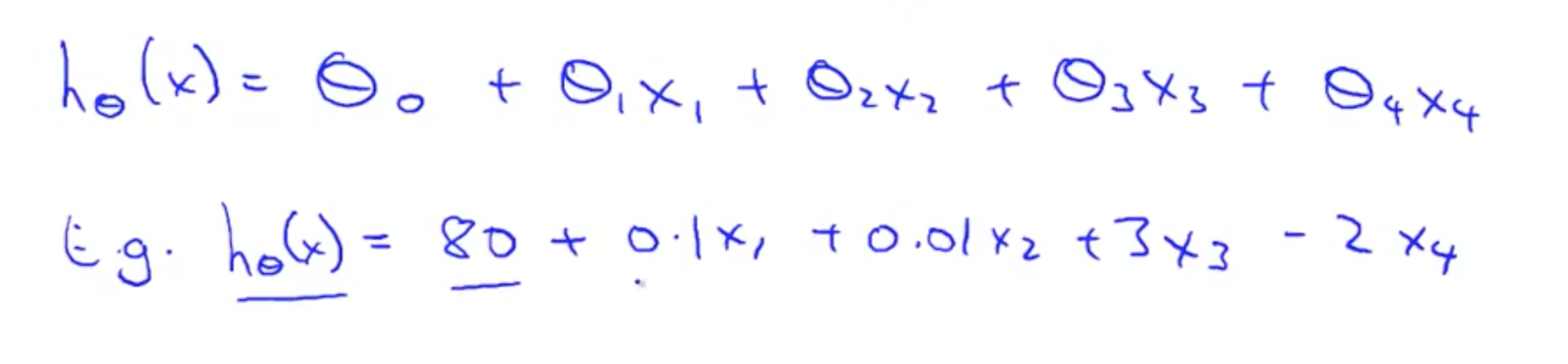

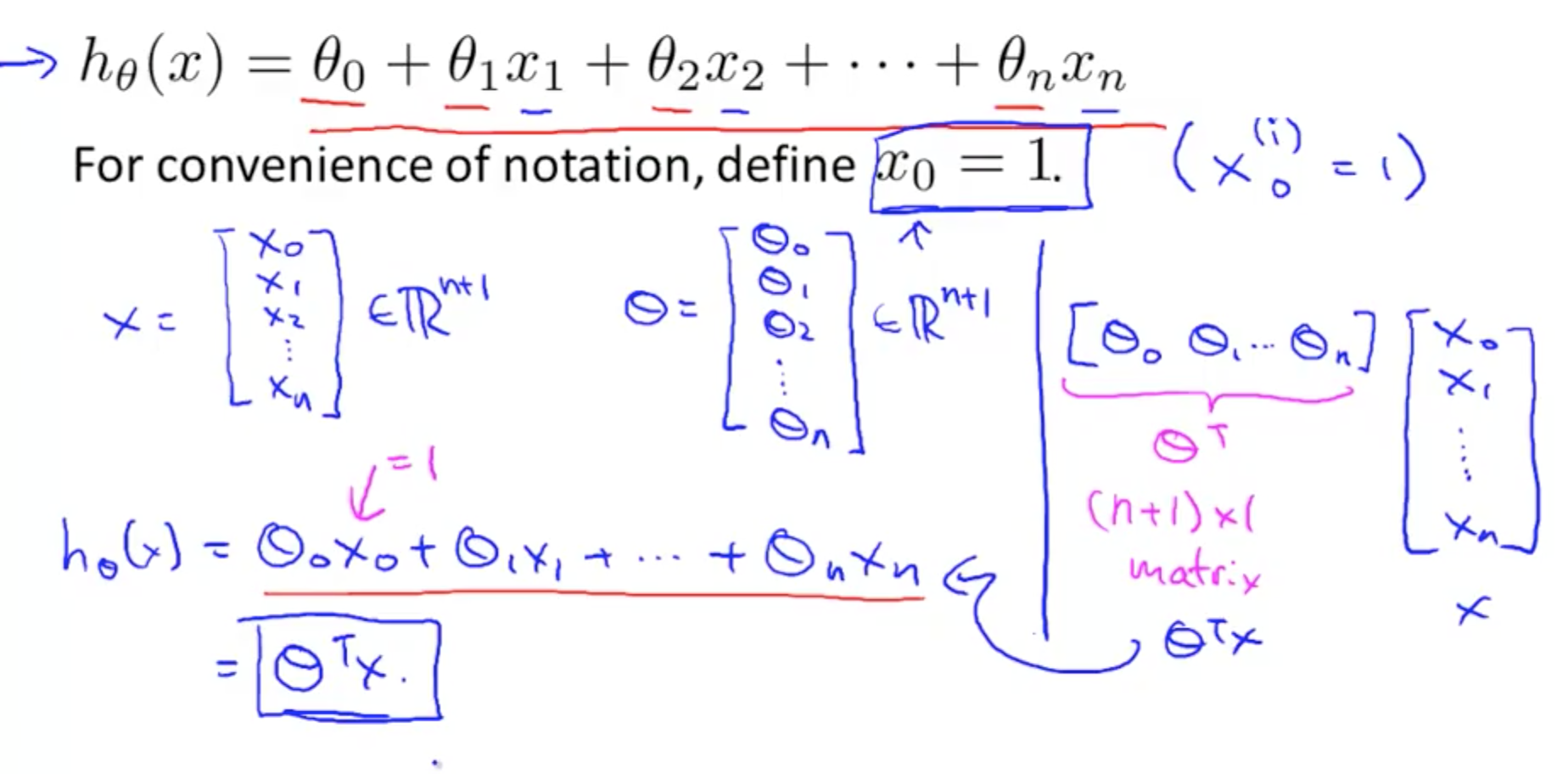

- New hypothesis

- Multivariate linear regression

- Can reduce hypothesis to single number with a transposed theta matrix multiplied by x matrix

- Can reduce hypothesis to single number with a transposed theta matrix multiplied by x matrix

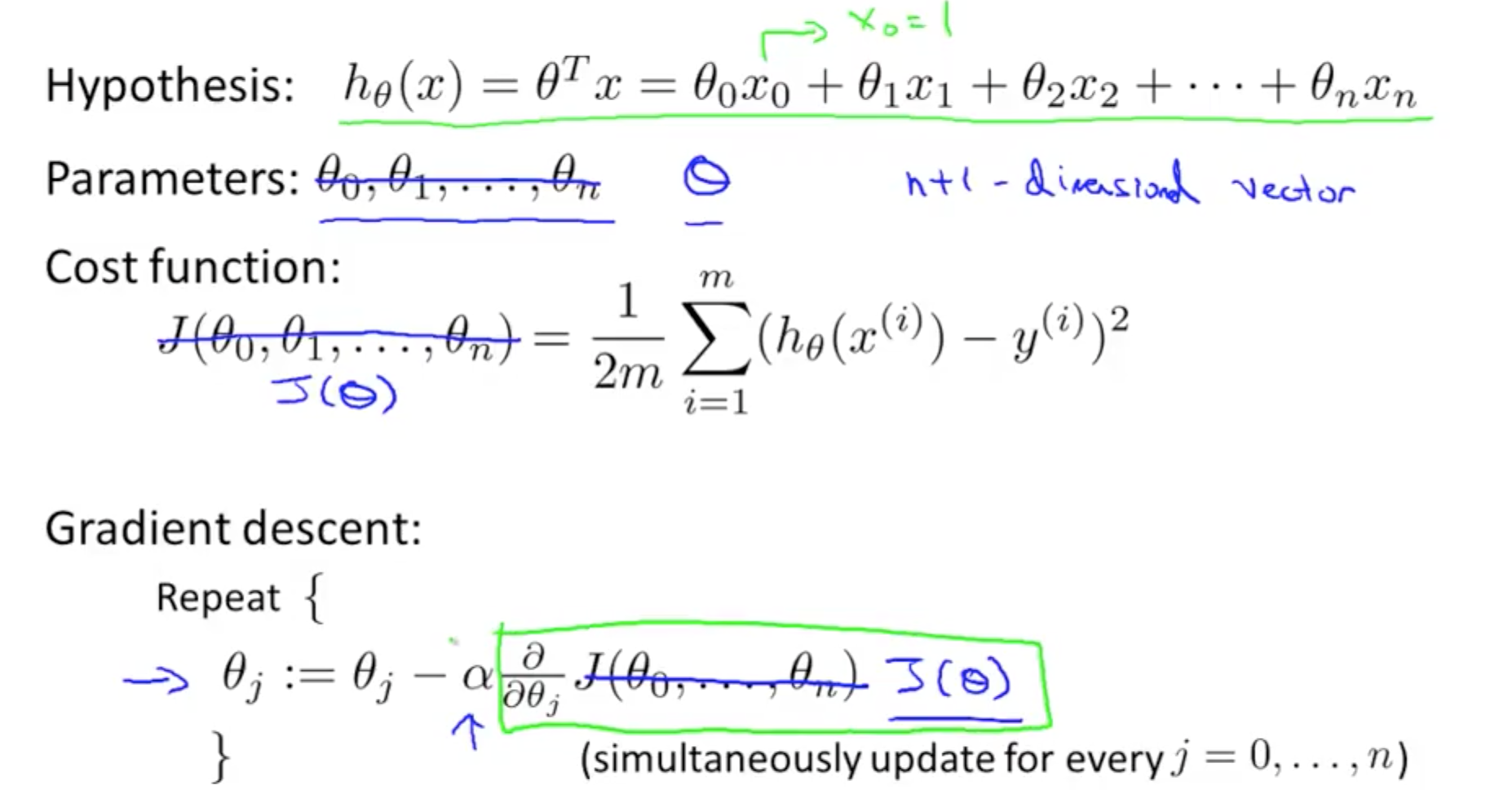

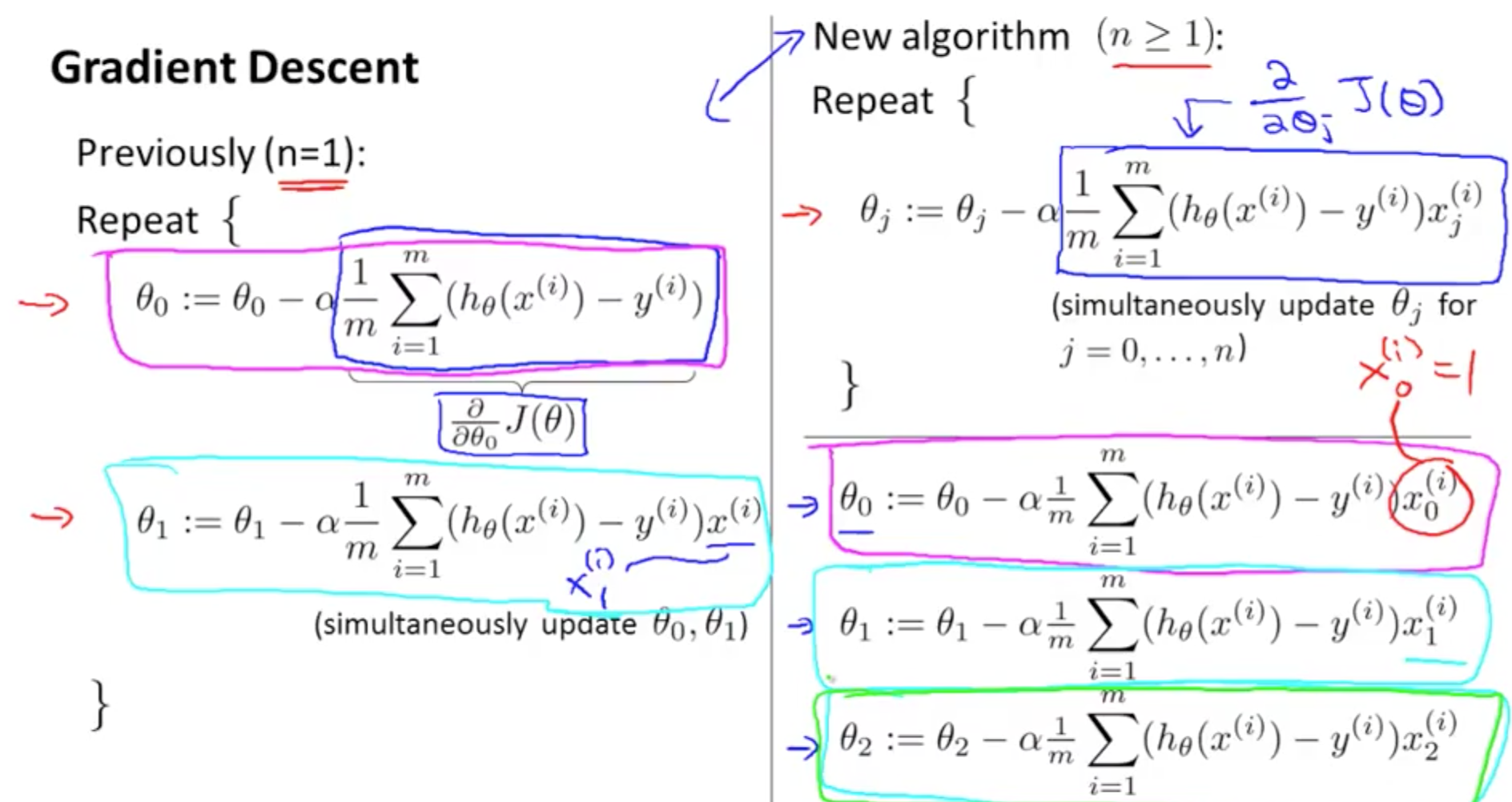

1b. Gradient Descent for Multiple Variables

- Summary

- New Algorithm

1c. Gradient Descent: Feature Scaling

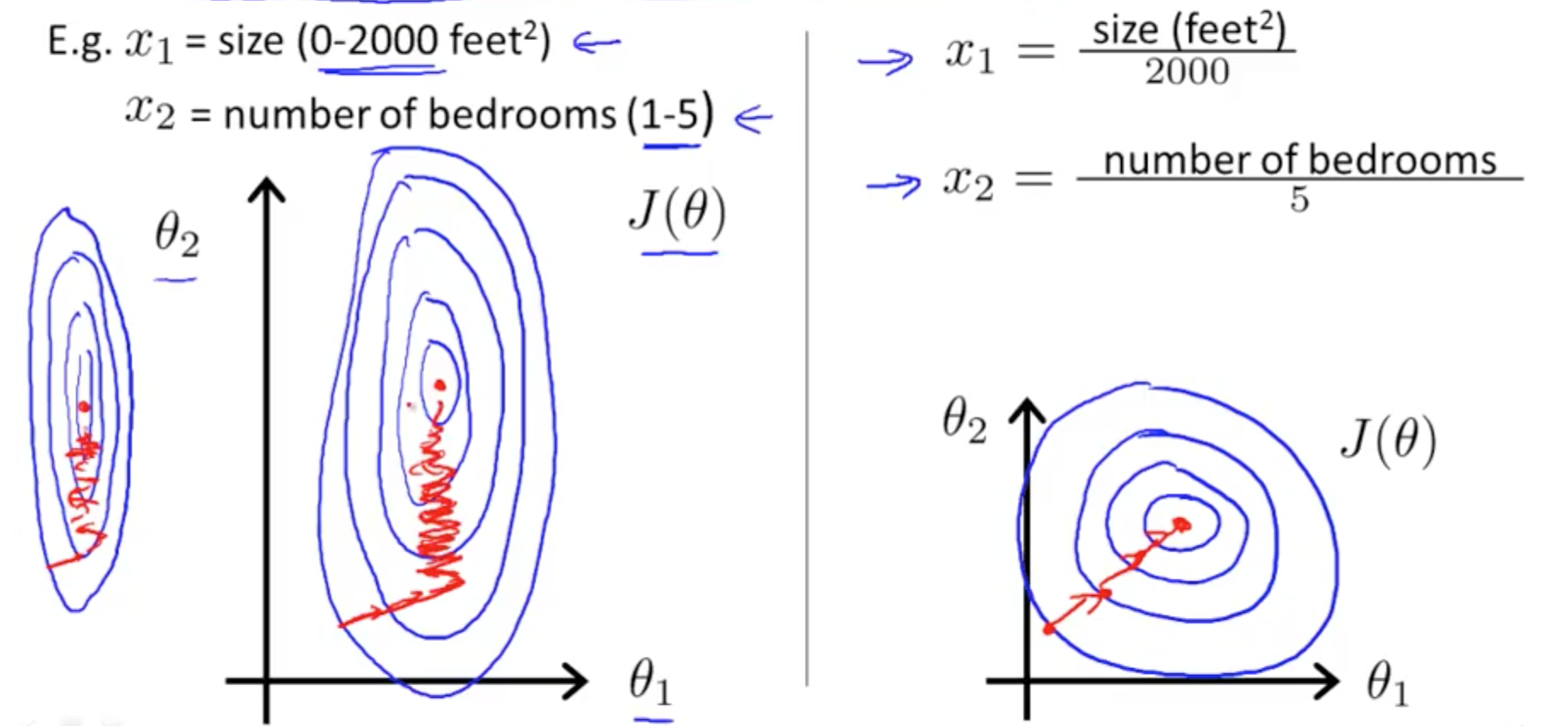

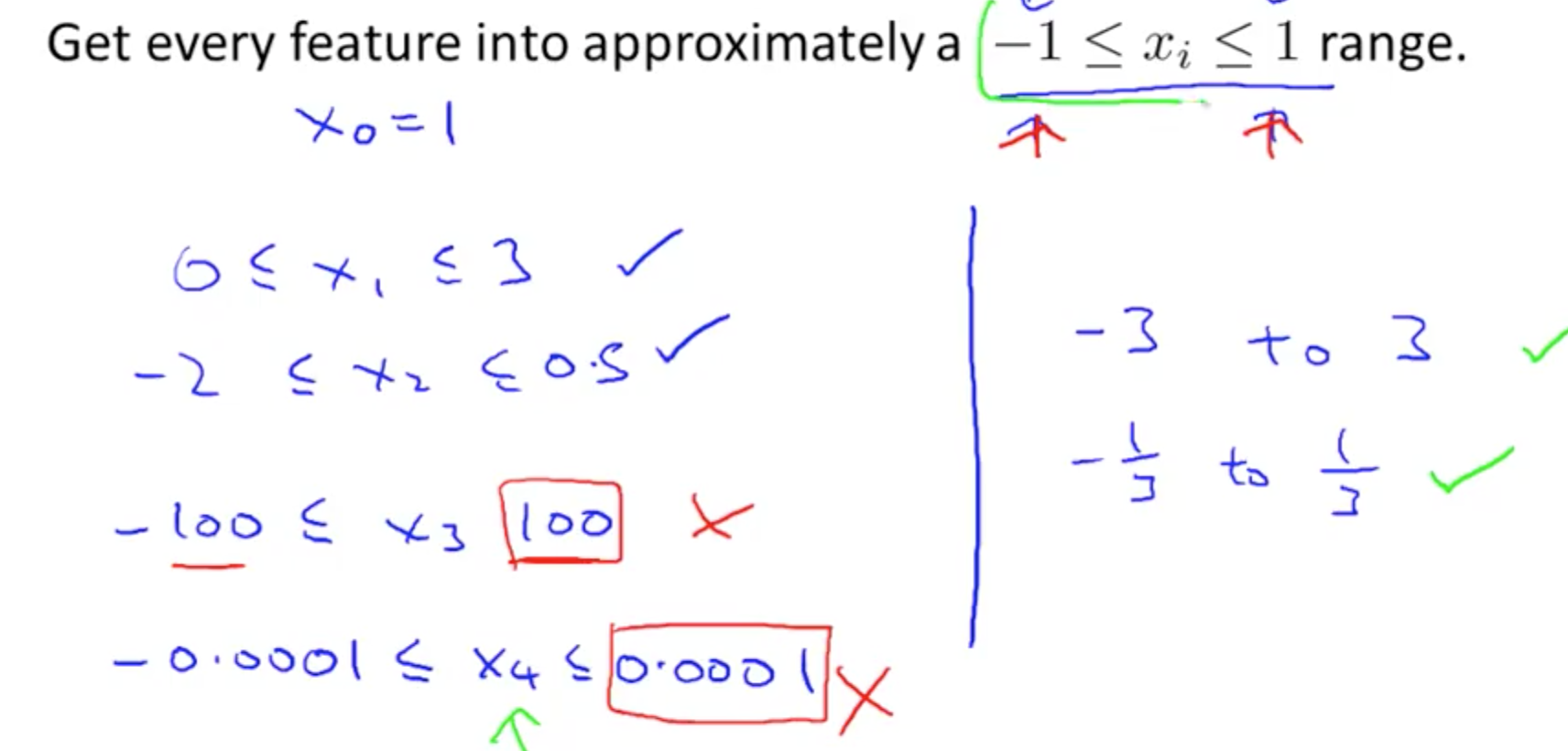

- Ensure features are on similar scale

- Gradient descent will take longer to reach the global minimum when the features are not on a similar scale

- Feature scaling allows you to reach the global minimum faster

- So long they’re close enough, need not be between 1 and -1

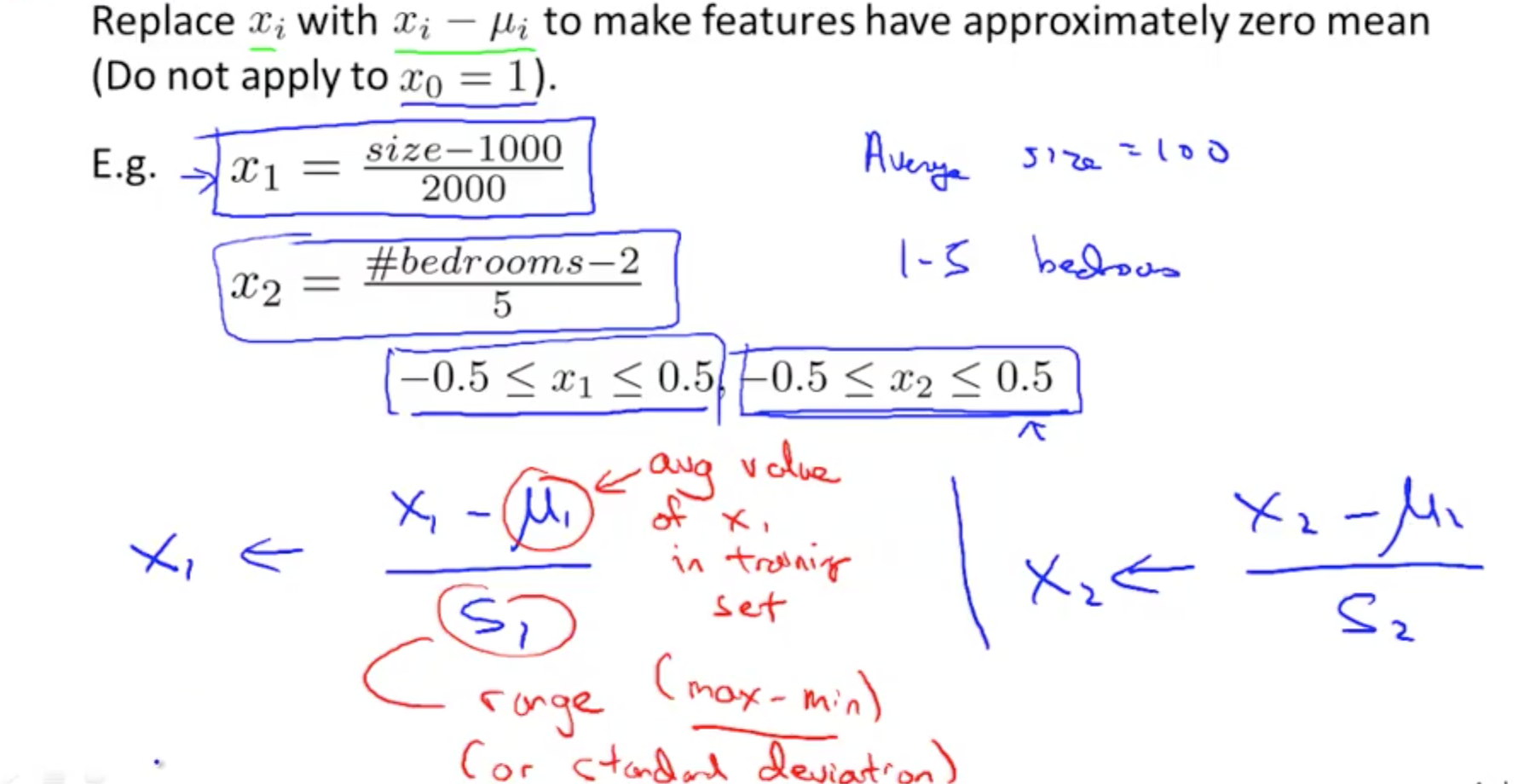

- Mean normalization

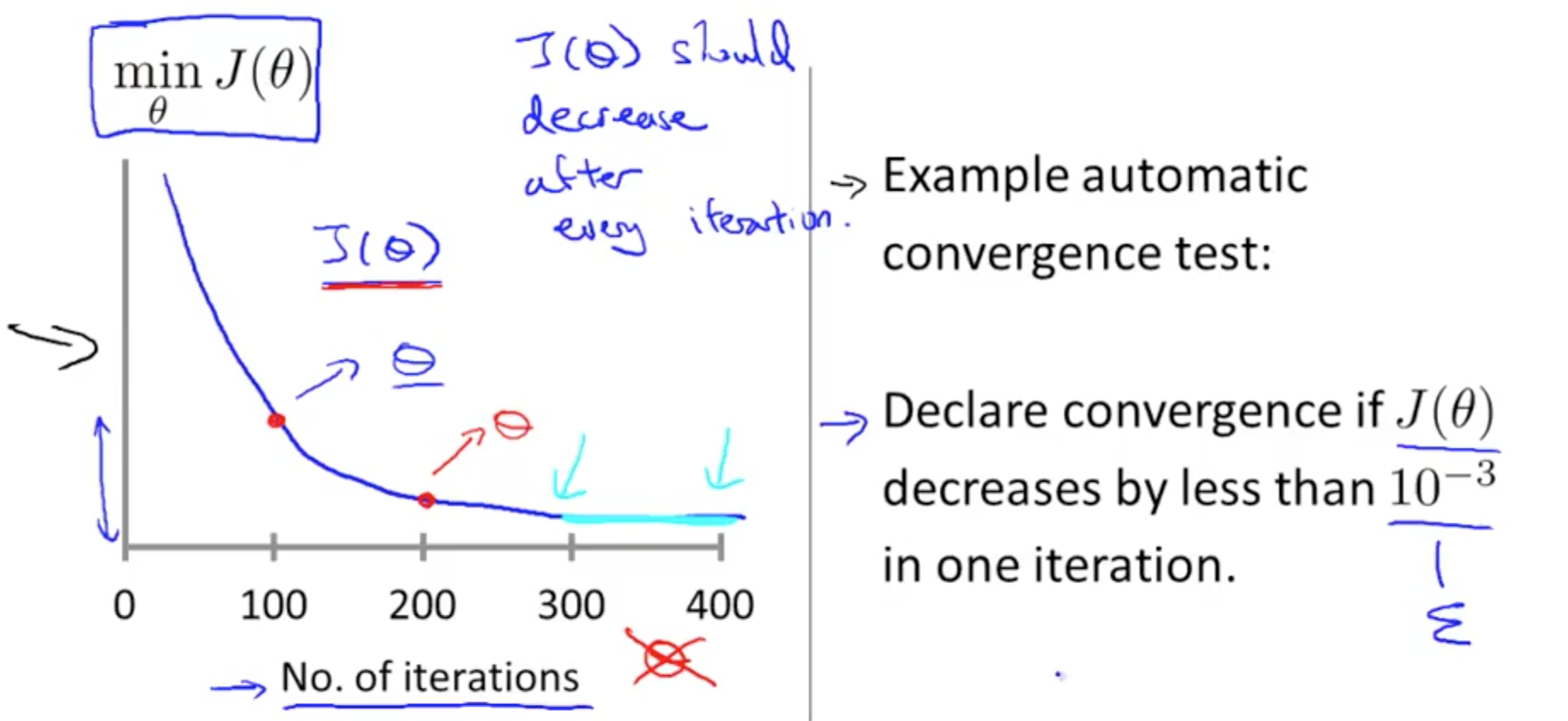

1d. Gradient Descent: Checking

- Can you a graph

- x-axis: number of iterations

- y-axis: min J(theta)

- Or use automatic convergence test

- Tough to gauge epsilon

- Tough to gauge epsilon

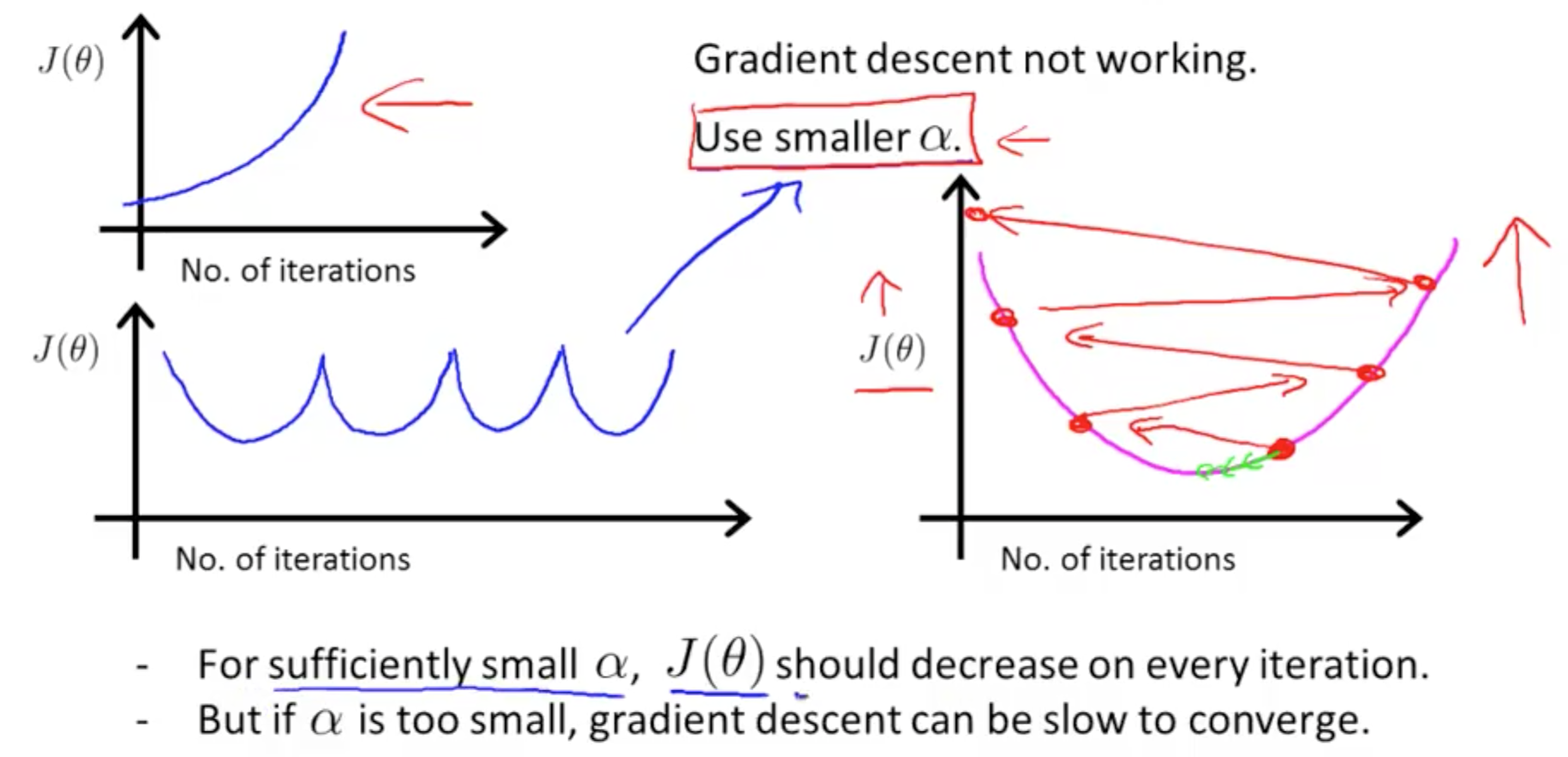

- Gradient descent that is not working (large learning rate)

1e. Gradient Descent: Learning Rate

- Alpha (Learning Rate) too small: slow convergence

- Alpha (Learning Rate) too large:

- J(theta) may not decrease on every iteration

- May not converge (diverge)

- Start with 0.001 and increase x3 each time until you reach an acceptable alpha

- Choose a slightly smaller number than that acceptable alpha value

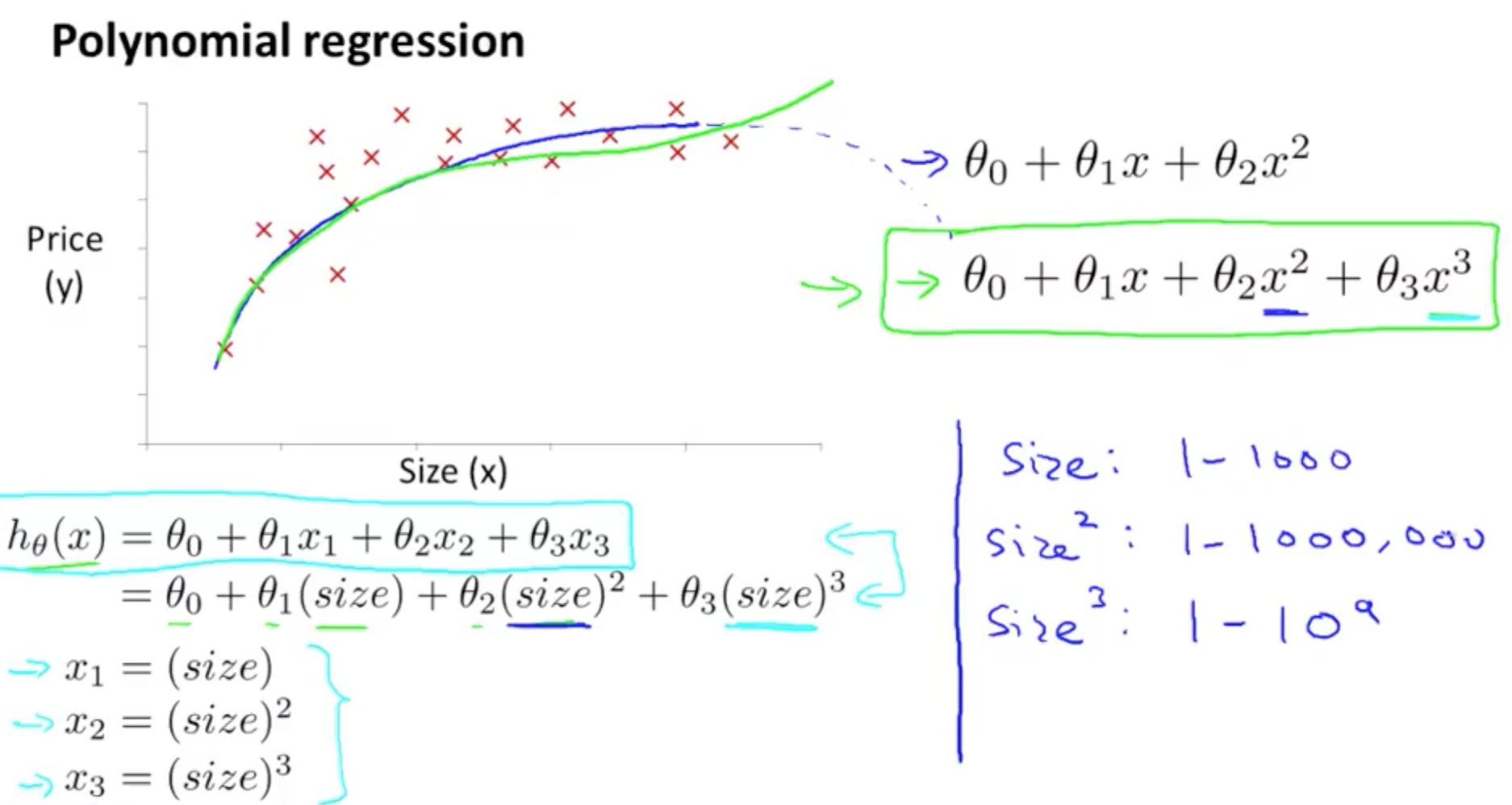

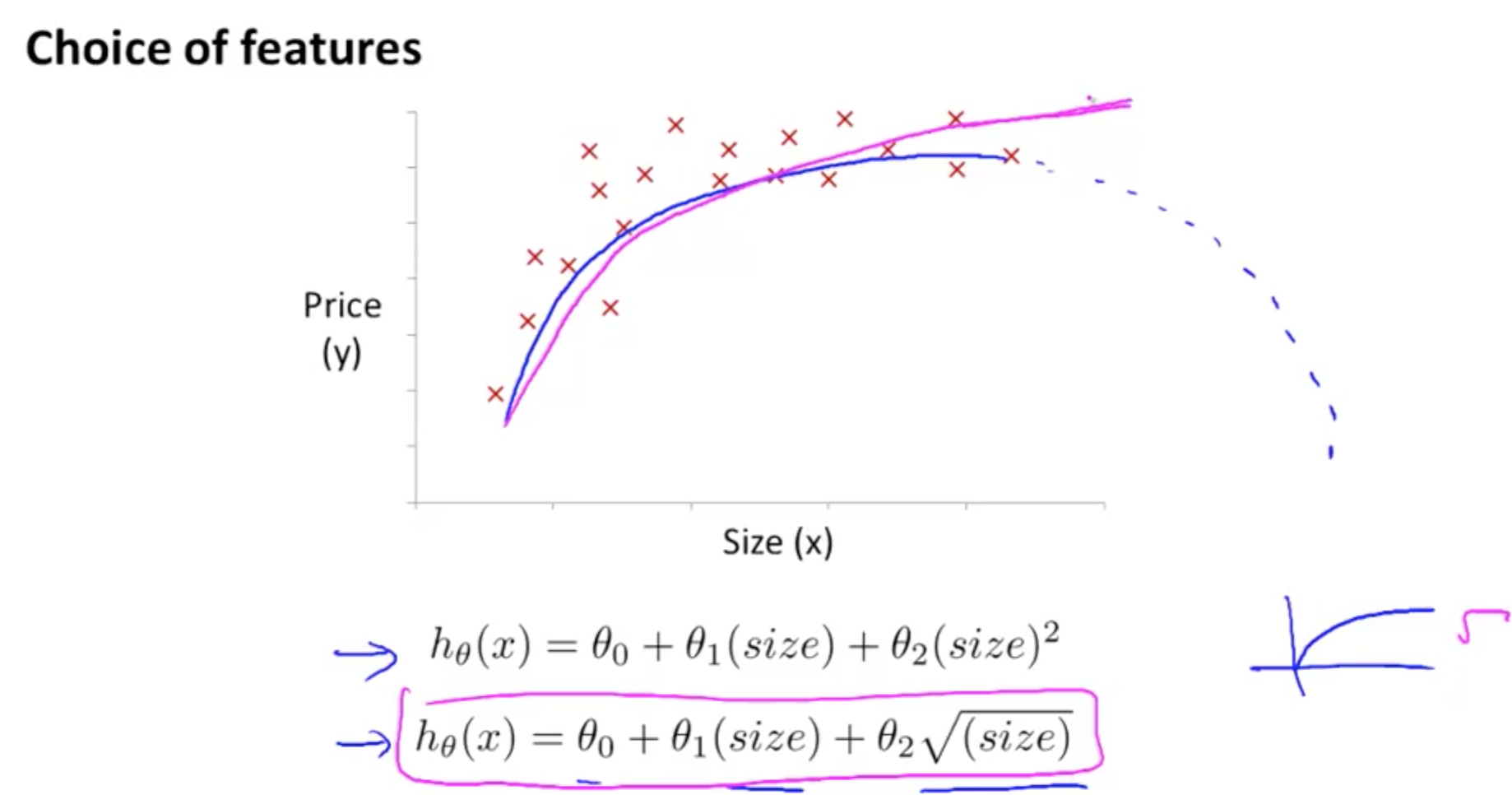

1f. Features and Polynomial Regression

- Ensure the features capture the pattern

- Doesn’t make sense to choose quadratic equation for house prices

- Use cubic or square root

- There are automatic algorithms, and this will be discussed later

2. Computing Parameters Analytically

2a. Normal Equation

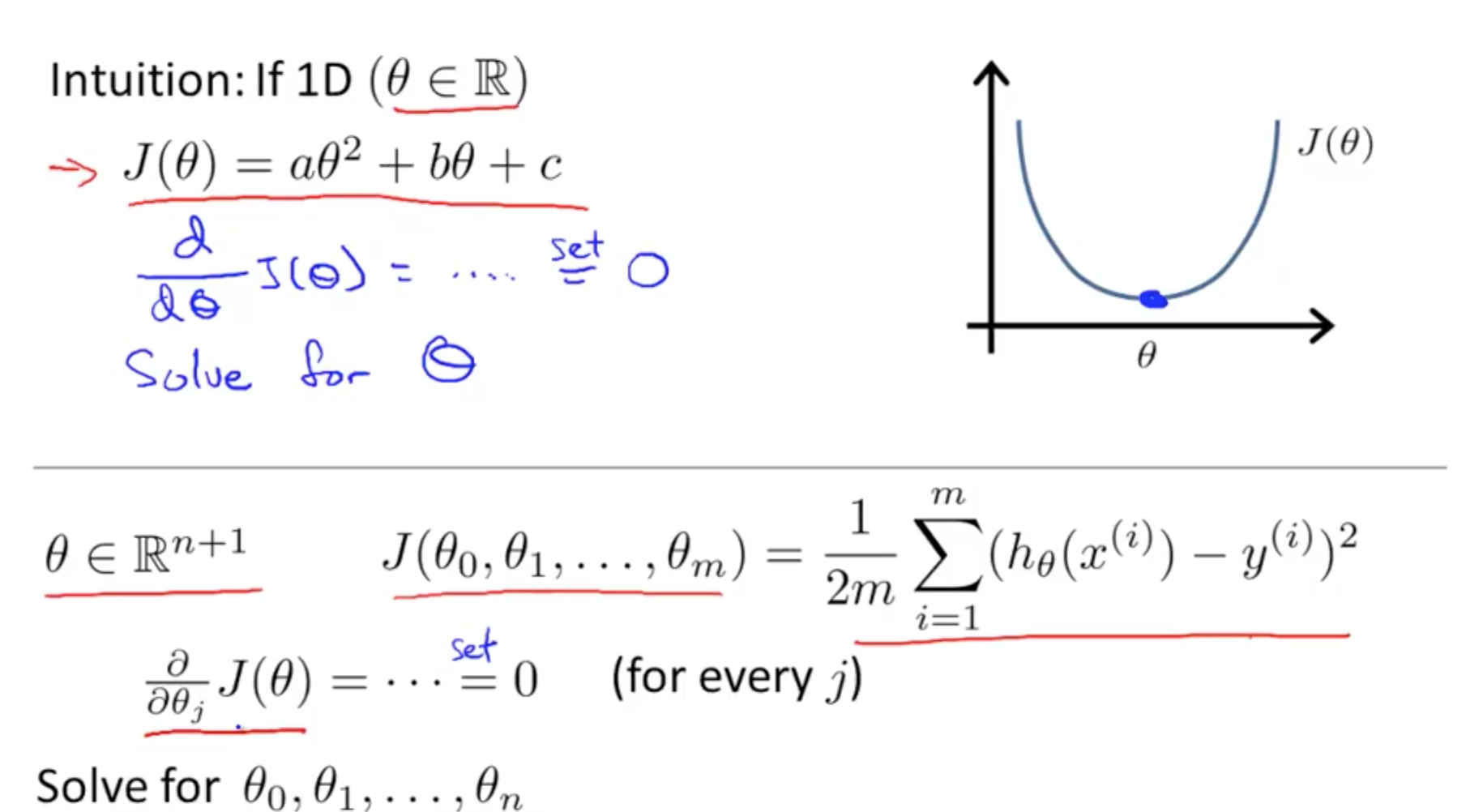

- Method to solve for theta analytically

- If theta is real number

- Minimise J(theta) is to take the derivative and equate to zero

- Solve for theta

- If theta is not

- Take partial derivative and equate to zero

- Solve for all thetas

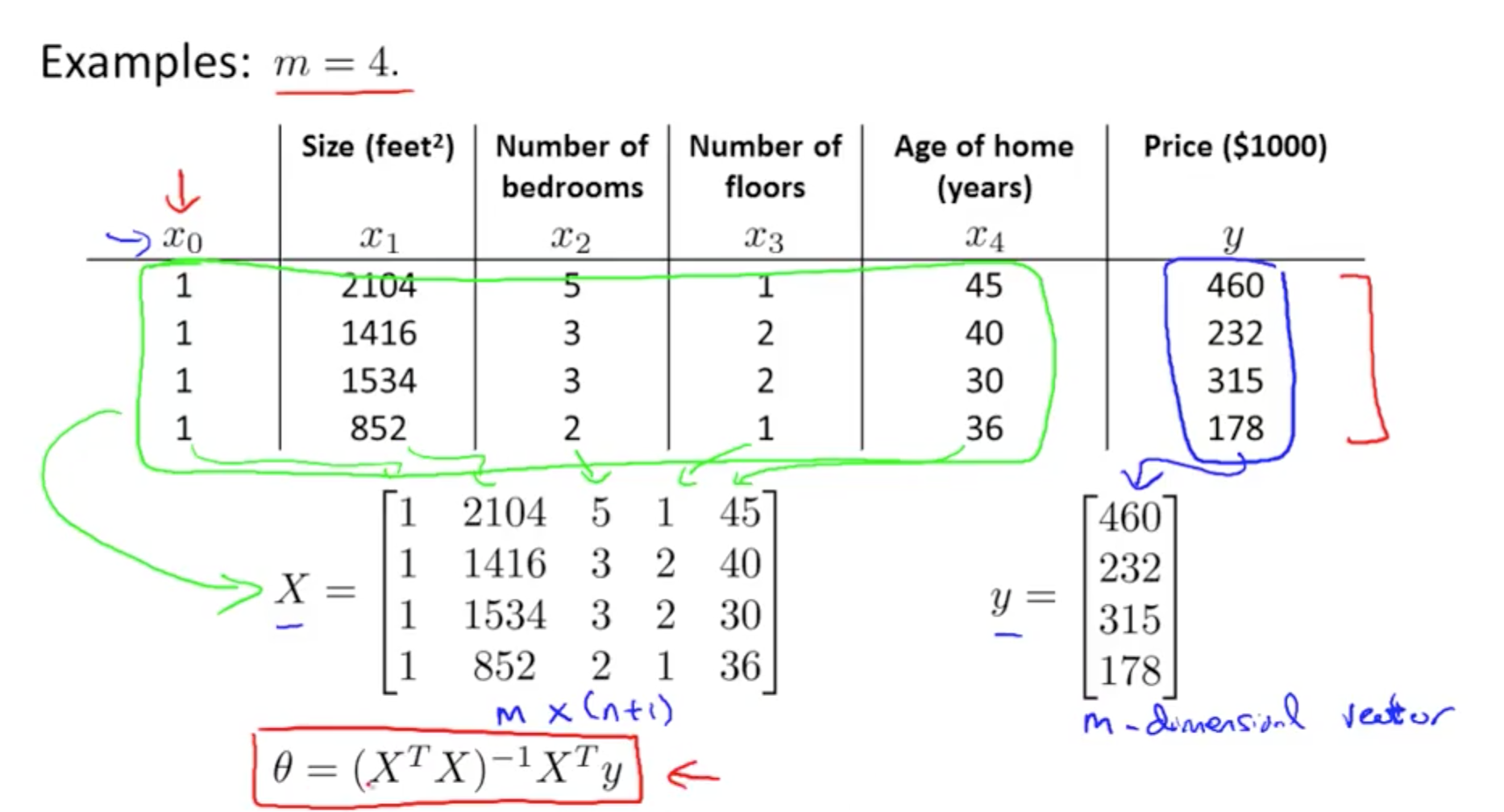

- Minimise Cost Function: Specific Example

- X: m x (n + 1)

- m: number of training examples

- n: number of features

- X_transpose: (n + 1) x m

- X_transpose * X: (n + 1) x m * m x (n + 1) = (n + 1) x (n + 1)

- (X_transpose * X)^-1 * X_transpose: (n + 1) x (n + 1) * (n + 1) x m = (n + 1) x m

- theta = (n + 1) x m * m x 1 = (n + 1) x 1

- X: m x (n + 1)

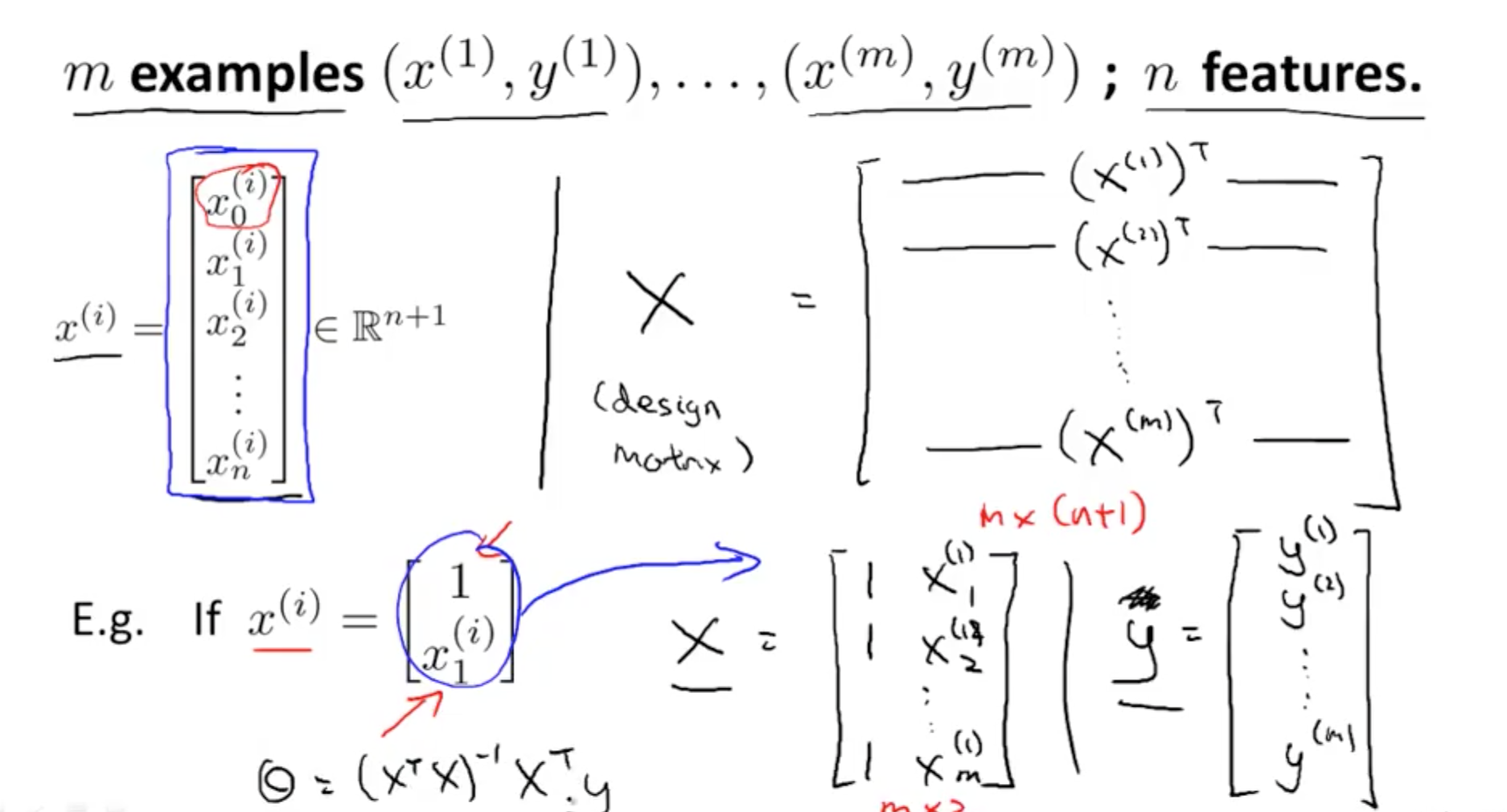

- Minimise Cost Function: General

- Minimise Cost: Octave Code

- No need for feature scaling using normal equation

pinv (X' * X) * X' * y

- Gradient Descent vs Normal Equation

| Gradient Descent | Normal Equation |

|---|---|

| Need to choose alpha | No need to choose alpha |

| Needs many iterations | Don’t need to iterate |

| Works with large n (10,000) | Slow if n is large (100, 1000 is fine) |

| Number of features > 1000 | So long number features < 1000 |

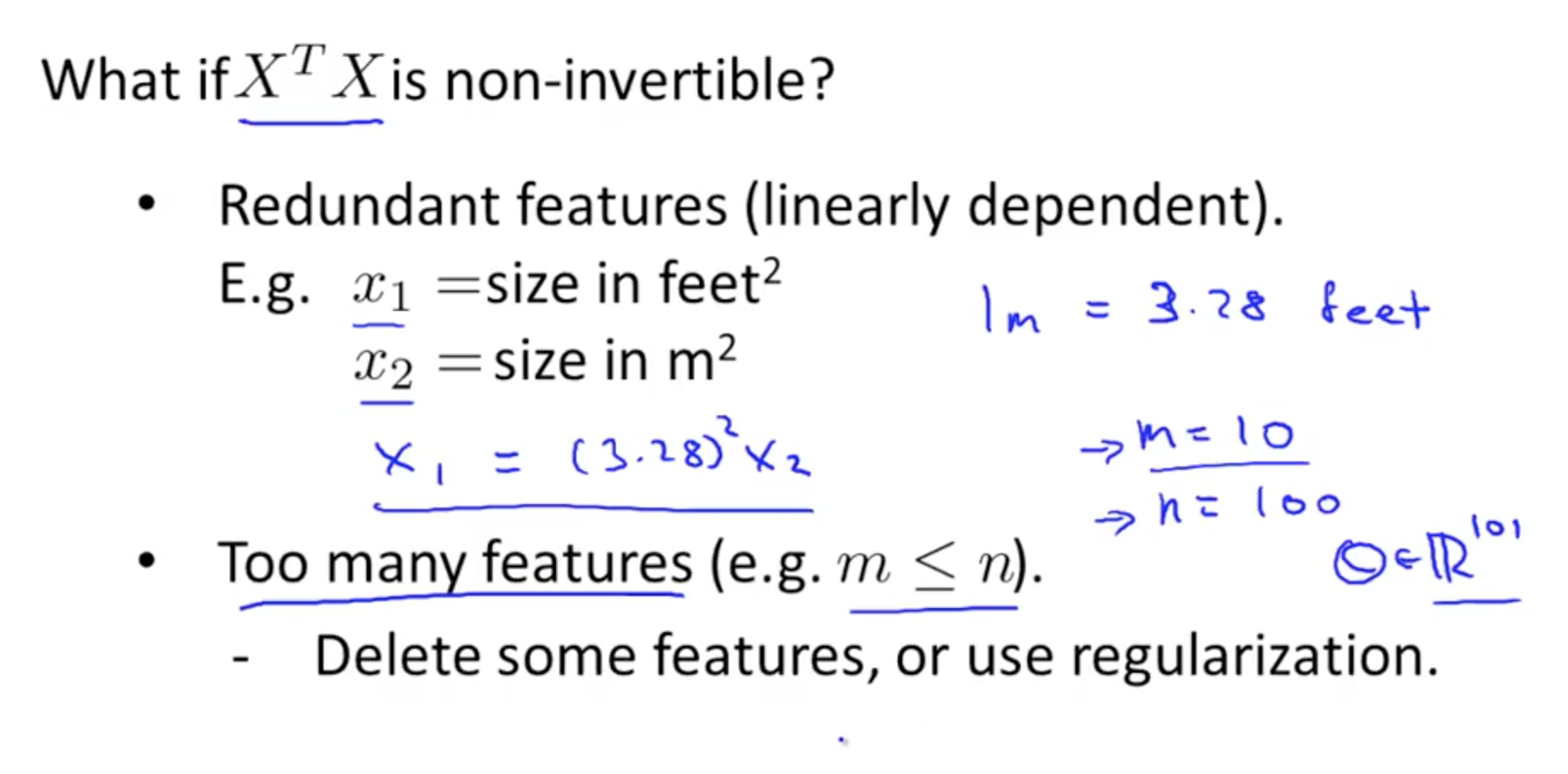

2b. Normal Equation Non-invertibility

- What happens if X_transpose * X is non-invertible (singular or degenerate)

pinv (X' * X) * X' * y- This works regardless if it is non-invertible

- Intuition of non-invertibility

- Causes of non-invertibility

- Delete redundant features to solve non-invertibility problem

- Delete some features or use regularization

- Causes of non-invertibility